Ivane Javakhishvili Tbilisi State University

Paata Gugushvili Institute of Economics International Scientific

BANKING BUSINESS MODEL ANALYSIS – METHODOLOGICAL APPROACH

Abstract. The analysis of the international experience assumes that the economic growth of a state is based on a well-developed banking system, oriented to an intensive risk-based supervision, to an evaluation of macroeconomic factors as well as to the evaluation of the impact it brings on the risks to which financial institutions are subject to. Evaluation of the banking business model with the aim of maximizing profit under the regulatory conditions imposed by the supervisor. Defining the elements of a banking business model and identifying risk that can result both from internal factors (such as inefficient design or pricing of key products, inadequate targets, reliance on an unrealistic strategy, excessive concentrations of risk, poor financing and capital structures or insufficient execution capabilities) and external factors (such as a challenging economic environment or a changed competitive landscape). The definition of a clear methodology for evaluating the banking business model in both quantitative and qualitative aspects, determines the possibility of early action, aimed firstly at evaluating banking performance by determining the solidity of the bank, its degree of exposure to various risk categories and then its level of efficiency.

Keywords: business model, analysis, viability, sustainability, quantitative and qualitative analysis

1. INTRODUCTION

According to the author, a business model represents the means and methods used by an institution to operate, generate profits and grow. Each business model is unique, although common business model characteristics can be found across institutions. These features refers to: (1) operating environment; (2) regulatory environment; (3) supervisory actions/measures; (4) resolution actions/measures; (5) internal factors/dependencies; (6) external factors/dependencies.

Globalization, the impact of the pandemic on global development, armed conflicts, hybrid wars, money circulation, the mobilization of all monetary funds in the economy and their management in order to carry out the normal social-economic activity, imposed a series of challenges in the configuration of a functional banking business model based on a market economy, adapted to international community regulations. The need to evaluate the banks' business model from the perspective of determining the profitability that the business model can generate. Thus, the importance of the early determination / ascertainment of the risks to which it is subject represents the primary stage in the development of the business model. Business model risk is defined as the bank's inability to generate adequate profit and growth in the course of business as an inherent fact of the institutions business model and not because of a specific risk. Risk can result from internal factors (such as ineffective design or pricing of key products, inappropriate targets, reliance on an unrealistic strategy, excessive concentrations of risk, poor financing and capital structures or insufficient execution capabilities) and external factors (such as a challenging economic environment or a changed competitive landscape).

The purpose of the paper: the development of the methodology for evaluating the banking business model in order to strengthen the stability of the banking system.

Research objectives: investigating the theoretical foundations of the assessment of the banking business model, the classification and characteristics of the elements of the business model, the stages and the analysis process as well as the actions after.

In developing of the methodology for evaluating the banking business model, the author relied on the following methodological benchmarks:

a) The conceptual framework for defining the assessment of the banking business model;

b) The research methods used in the development of the business model evaluation methodology;

c) Research results for the development of the banking business model evaluation methodology and application conclusions.

The methodology developed by the author includes the following components:

2. THE CONCEPTUAL FRAMEWORK

The assessment of the banking business model have to determine: viability which is not less than 12 months and sustainability, which refers to the ability of an institution to generate acceptable returns from a supervisory perspective over a period of three years and through a whole cycle. Investors tend to be concerned with whether the returns are acceptable compared to the cost of equity. From a supervisory perspective, it is more important that returns come from an appropriate funding and capital structure and an appropriate risk appetite over a full business cycle. Business model assessment is therefore the process that allows the supervisor to understand the operation of the institution in a future-oriented manner. Supervisory assessment is usually a combination of qualitative knowledge and quantitative analysis. Any business model element is accompanied by certain characteristics, as well as associated business risks and vulnerabilities.

The main elements of a banking business model are:

- Ø The activities that the bank practices. They are retail oriented, transaction oriented, specialized bank or universal bank characteristics. The associated risks and vulnerabilities refer to credit risk, transformation risk (specific to retail sales), market risk, counterparty risks (specific to trading orientation), contagion risk, complexity (associated to the specialized bank) and concentration risk (specific universal bank);

- Ø Resources (capital and structure of funding) / liquidity profile. This element is characterized by: predominance of wholesale funding (freeze of market founding, volatility of founding), the predominance of retail deposits, high leverage (reliance on external funding), predominance on encumbered funding (difficulty in liquidation, reduced resilience in times of crisis, less eligible collateral), predominance of short-term funding (high risk illiquidity, combined with long-term assets, high risk of maturity mismatch);

- Ø Structure of income. Income can be from interest, from trading, as well as from non-diversified sources of funding. The predominance of interest income also entails interest rate risk, those from transactions are accompanied by the vulnerability of income volatility, and those from non-diversified financing sources - depend on the absorption of the gain;

- Ø Geographical scope implies the orientation of the bank towards to large foreign exposures or to domestic focus. In the case of external exposure, the entity will face currency risk, political risk and country risk. In the case of internal activity, the imminent risk remains that of concentration;

- Ø Size. In the case of a large size, the banking entity faces systemic risk, excessive risk appetite ("too big to fail"), and in the case of a small size – weaker resilience;

- Ø Originate to hold / to distribute. When lenders make loans with the intention of selling them to other institutions and/or investors, as opposed to holding the loans until maturity. In the case of high use of securitization, lenders encounter difficulties regarding the lack of credit standards and / or knowledge regarding the creditworthiness of borrowers, opacity, increased risk appetite. The limited use of securitization implies an increased credit risk as well as the presence of transformation risk;

- Ø Risk appetite and performance. The presence of a high risk appetite leads to the probability that the business model is unsustainable. In addition, the risk of solvency and profitability may arise with the possibility of losing all profit;

- Ø Operational structure and governance (organization and expansion into multiple subsidiaries and branches or organization into interdependent and centralized entities). The first form of organization is accompanied by operational risk, management risk and is too complex to manage, while the second form of organization presents an increase in the risk of contagion.[1]

Table no. 1. Banking business models:

classification and characteristics of the defining elements

|

Business model |

Business model element |

|

|

Activity |

Resources |

|

|

Cross-border universal bank |

Engaged in several banking activities Major cross-border operations |

Diversified source of funding Significant funding foreign investors Both taking and not taking retail deposits |

|

Local universal bank |

Engaged in several banking activities Operating predominantly in their domestic market |

Diversified source of funding predominantly in domestic market |

|

Consumer credit banks (including automotive banks) |

Originating and servicing consumer loans to retail clients |

No specification |

|

Co-operative banks / savings and loans associations |

Originating and servicing loans to local community individuals and businesses (excl. diversified co-operative banks) |

Retail deposits

|

|

Mortgage banks taking retail deposits |

Originating and servicing mortgage loans to retail clients (incl. Bausparkasse) |

Retail deposits |

|

Savings banks |

Retail banking for individuals and SMEs |

Retail deposits |

|

Institutions not taking retail deposits (including pass-through financing) |

Originating and servicing loans Includes pass-through financing |

Issuance of covered bonds or other types of securities liabilities |

|

Private banks |

Wealth management services to high net worth individuals and families |

No specification |

|

Corporate-oriented |

Specialized in financial services for businesses, domestic and international trade, leasing (asset-backed financing) and/or factoring activities, project finance. (incl. Landesbanken ) |

No specification |

|

Custodian institutions (including CSDs, that are subject to CSDR) |

Custodian services and other services such as account administration, transaction settlements, etc. |

No specification |

|

Other specialized banks |

Banks not included in the above categories (residual category): - Public development banks - Islamic finance - Co-operative central banks - CCPs |

No specification |

Source: Developed by the author based on data from Cernova M. and Urbano T., (2017), Identification of EU bank business models

3. RESEARCH RESULTS AND DISCUSSIONS

Business model analysis is a supervisory activity undertaken by supervisors to contribute to the development of an insight into the current business model of the supervised institution and its viability, establishing how the business model may evolve as a result of the strategic choices made by the institution and / or the impact of changes on the business environment in which it operates and therefore its sustainability.

The objectives of the business model analysis are:

- Assessment of the viability of the current business model;

- Assessment of the sustainability of the strategy;

- Help to identify key vulnerabilities.

It is important to specify that the business model analysis does not undermine the responsibility of the bank's management body for the organization and management of the business and does not seek to introduce supervisory ratings or preferences for different business models.

The analysis of the business model starts from the framing of the entity's activity in the legal norms of activity and the community regulations. Monitoring key indicators, assessing internal governance and institution-wide controls is the next step. The assessment of the banking business model is based on the capital risk assessment and the liquidity and funding risk assessment. Assessment of inherent risks, determination of equity requirements, liquidity requirements, capital adequacy assessment, liquidity adequacy assessment and stress testing represent the monitoring of key indicators. The overall assessment of the system involves the imposition of certain supervisory measures, namely quantitative capital measures; quantitative measures of liquidity; and other surveillance measures.

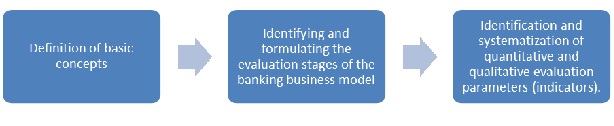

The business model analysis process can be described in three stages.

Figure 1. Stages in Business model analysis process

Source: Created by the author based on Regulation on Banking Activity Management Framework No. 322 of December 20, 2018б Official Monitor of the Republic of Moldova No. 1-5, Article 56 of January 4, 2019

- Ø Preparation. At this stage, the primary assessment takes place, the identification of the focus of the model analysis as well as the assessment of the business environment;

- Ø Execution. Quantitative and qualitative analysis of the current business model, analysis of the forward-looking strategy and financial plans (including changes planned to the business model);

- Ø Drawing conclusions and actions. Formation of surveillance visualization, including model analysis score, outcomes of the assessment (supervisory strategy, addressing threats to viability and sustainability).

The stages of preparing the business model analysis are: (1) preliminary assessment – determination of materiality of certain business lines/ products, identification of peer groups (based on business lines/ product lines), support categorization of institutions; (2) scoping – whole institution (group), material entities and group add-up, major business lines / product lines; (3) assessing business environment – regulatory trends, macro-economy, technological trends (fintech), investor appetite, customer behavior.

Fintech represents a very important component in the assessment of the business environment. For banks, FinTech means rethinking the interaction with customers, improving the customer experience through the use of innovative technologies, using new technologies for digitalization, optimizing internal processes, a component of continuous transformation. With the development of Fintech in the banking sector, the entity acquires new opportunities, but also risks, the main ones being presented below:

Figure 2. Fintech risk in banking sector

Source: Developed by the author based on De Nederlandsche Bank (DNB) presentation at the EBA SGV: The impact of technological innovation on the financial sector – DNB research.

Business model analysis focuses on how the institution makes a profit, what the key drivers of profitability are, how the bank intends to make a profit in the future, and how the key drivers of profitability will change. To determine them, the bank analyzes the current business model from a quantitative and qualitative point of view, as well as the future strategy to achieve the desired performances. The quantitative analysis is based on the analysis of the profit and loss ratio, the balance sheet and the risk appetite. Assessment areas include: profitability in context, sources of income and losses, sources of costs, sources of impairments, income distribution, assets structure, quality and riskiness of assets, structure and riskiness of funding, adequacy and appropriateness of capital bases, structure and riskiness of off-balance sheet exposures, capital and liquidity structure of the group, risk appetite. Qualitative analysis is based on: execution and risk management capabilities (ongoing ability of the organization including management to deliver), key external dependencies (third party provides, intermediaries and partnerships, regulatory changes, stakeholder support), key internal dependencies (distribution structures and channels , IT systems / platforms, operation and resource capacity), franchise (brand recognition and awareness, overall brand strength, customer loyalty), areas of competitive advantage (competitive advantages, global network, economies of scale, product mix and proposition).[2]

The quantitative and qualitative analysis approach applies both to the evaluation of the current business model and the future strategy (financial projections). It is necessary to build a picture of the institution's current business model and to gain an insight into its viability. The main objective of the business model analysis is to form a vision of the sustainability of the institution's business model, as it forms the basis for issuing forward-looking supervisory judgements to address potential emerging risks.

The tools used in the evaluation of the banking business model can be divided into three main directions: back-end, front-end and reports.

Back-end for the assessment of the banking business model involves the function of preparing surveillance data, macroeconomic data and forecasts, cluster calculation for defining / confirming current and future business models, as well as for benchmarking. Also included in this evaluation category is the forecasting of the balance sheet and Profit Losses elements based on stable estimates at the bank level and the use of machine learning techniques (LASSO approach) with the ability to synchronize the system and corrections. Estimations are subject to supervisory scrutiny (expert corrections, results from more detailed models).

Front-end for the assessment of the banking business model is based on communication with R (VBA macros that directly run R code via the BERT plugin), data management function (import, export, upload), environment setup (configuration of key functionalities and libraries used in online and offline mode), template structure (configuration of template / report structure along with charts, summary sheets, detailed calculations), clustering configuration (definition of clusters used for benchmarking), export function (creation and export of bank level reports).

Reports consist of bank level reports (historical and forecast figures for each individual bank), aligned supervisory data (individual level data from Matrix reporting and COREP & FINREP fully aligned with BS Health card), the multilateral uses (top-down computations, enriched with bottom-up supervisory knowledge, used for bank forecasting challenges, analyzing their profitability, and bank-level hypothesis testing).

The key actions of the business model analysis are:

- business model analysis allows a holistic view of an institution, focuses on the business model, strategy and key vulnerabilities;

- the analysis is versatile and can be conducted on the level of the institution / business line / product line / specific theme, all with different action groups;

- the economic context is very important, the macro-economic environment affects both the current model and the plausibility of the strategy;

- the analysis is not mechanical and respects the supervisory judgement, the importance of dialogue with an institution;

- the results of the business model analysis can lead to surveillance measures and early intervention measures, without undermining the institution's own responsibility for business management;

- the analysis is related to the evaluation of SREP (Supervisory Review and Evaluation Process) elements, as implications from other areas such as capital and liquidity can also be identified.

Table no. 2. Business models components and indicators

|

Business model elements |

Business models components and indicators |

|

1. Activities (assets structure)

|

|

|

2. Resources (capital and structure of funding) |

|

|

3. Structure of income |

|

|

4. Geographic scope |

|

|

5. Size |

|

|

6. Originate to hold/to distribute |

|

|

7. Risk appetite and performance |

|

|

8. Liquidity profile |

|

|

9. Operational structure and governance |

|

|

10. Medium term plans and strategy |

|

Source: Developed by the author based on the EBA Subgroup on Vulnerabilities (SGV), on Bank Business Models: Bank Business Models - Definition Evolution and Challenges

4. CONCLUSIONS

The global financial crisis, the COVID 19 pandemic, military conflicts and hybrid wars have highlighted the need for a solid methodology to evaluate the banking business model. Evaluating the business model in the early warning system, determining the potential impact of some external environmental factors (macroeconomic environment, regulatory changes, technological changes, climate change) on the elements of a bank's business model, examining the viability and vulnerability of different banks (strategy , financial results, indicators, assets quality, etc.), requires the existence of a detailed assessment of the business model to ensure the expected results are achieved. The need to evaluate the banks' business model arises from the perspective of determining the profitability that the business model can generate. In this context, it is important to determine / ascertain within the control, which data are used and are the basis for the development of the business model.

The services of banks, the methods of providing services by them, are in the process of transformation generated by the technical progress that modern society is going through. Therefore, the business models of credit institutions are adapted taking into account these changes. At the same time, were mentioned aspects which, for banks, are real challenges in modeling the business model, namely: (1) regulatory requirements, which have become more and more sophisticated - they generate additional costs, undermine businesses that were attractive and oblige banks invest in data, tools and processes; (2) macroprudential measures imposed by the supervisory authorities that lead to unfavorable consequences from the point of view of the profitability of the credit institution; (3) a low interest rate environment and the cost of compliance – low net interest margins and minimal fee income are damaging the traditional business; (4) customer needs and competition; (5) digitization of services.

The need to define a banking business model arises from the importance of ensuring the financial stability of the banking sector, which is a preliminary condition for the financial system to provide quality lending services characterized by the lack of imbalances that could cause a negative correction of the financial markets, the appearance of a financial crisis systemic or the inability of financial institutions to maintain the uniform performance of financial operations. The success of a banking business model is ensured by a solid methodology for evaluating this model through early actions aimed to evaluate banking performance by determining the bank's solidity, its degree of exposure to various risk categories and then the level of its efficiency.

References

- EBA Subgroup on Vulnerabilities (SGV) paper on banks’ business models: Banks business models - definition evolution and challenges;

- Cernova M. and Urbano T., (2017), Identification of EU bank business models;

- Regulation on Banking Activity Management Framework No. 322 of December 20, 2018б Official Monitor of the Republic of Moldova No. 1-5, Article 56 of January 4, 2019;

- De Nederlandsche Bank (DNB) presentation at the EBA SGV: The impact of technological innovation on the financial sector – DNB research;

- SECRIERU, A., LOPOTENCO V., PÂRȚACHI I. et al. Impactul adaptării sistemului financiar din Republica Moldova la standardele Uniunii Europene (monografie), Academiade Studii Economice a Moldovei. Chişinău, 2020. 198 p. ISBN 978-9975-3389-1-2;

- VIPHINDRARTIN, S., ARDHANARI, M. et al. Effects of Bank Macroeconomic Indicators on the Stability of the Financial System in Indonesia. In: Journal of Asian Finance, Economics and Business, vol. 8, No 1, 2021, pp. 647-654. ISSN 2288-4637.

- Ayadi, Rym and Pieter De Groen (2014), Banking Business Models Monitor 2014: Europe, CEPS Paperbacks.

[1] EBA Subgroup on Vulnerabilities (SGV) paper on banks’ business models: Banks business models - definition evolution and challenges

[2] SECRIERU, A., LOPOTENCO V., PÂRȚACHI I. et al. Impactul adaptării sistemului financiar din Republica Moldova la standardele Uniunii Europene (monografie), Academiade Studii Economice a Moldovei. Chişinău, 2020. 198 p. ISBN 978-9975-3389-1-2.